UNIKO Review: A Clear Look at the Platform, Owners, and Compensation Details

UNIKO review matters if you explore new investment options in crypto or DeFi. This platform presents itself as an advanced liquidity engine with smart features for steady returns. Yet many details stay hidden. We at Scams Radar pulled together every key fact from available sources to give you a straight, easy-to-follow picture. We focus on the owners, their backgrounds, and the full compensation setup. No hype. Just facts in plain English.

Table of Contents

Part 1: Who Owns UNIKO and What Is Their Background?

Ownership sits at the heart of any solid platform. Here, things feel unclear from the start.

The name links to Unico Capital AG, a company registered in Wil, Switzerland, on April 29, 2024. This makes it a very young entity. Its official purpose is simple: buying, holding, managing, and selling shares in other businesses. It acts as a holding company, not a full financial or trading firm.

Paid-up capital stands at only CHF 50,000. That amount is small when the platform talks about managing millions in an insurance pool or handling large total value locked (TVL). Two directors lead it: Cedric Nagel and Danilo Drmanic. Public records show no deep experience in quantitative trading, blockchain tech, or running big financial operations. Their profiles do not list past roles at major hedge funds, crypto exchanges, or similar institutions.

On the website itself, no team bios appear. No LinkedIn links, no photos, and no verifiable names for developers or executives. This anonymous approach stands out because legitimate projects usually share clear backgrounds to build trust.

Other businesses share similar names in Australia, Indonesia, Denmark, and Turkey. The Australian one focuses on loans and property finance, but it has no connection to this platform. The overlap can confuse people and add to the sense of unclear identity.

In short, the legal side points to a brand-new holding company with limited capital and directors whose experience does not match the sophisticated DeFi story presented online.

1.1 Compensation Plan and How Returns Work

The platform does not publish a full, step-by-step compensation table like classic referral programs. Instead, it uses a layered token system built around three coins: QUSD (stable base), BULX (liquidity provider with fee shares), and PAI (governance and staking rewards).

Value flows upward through these layers. Users stake or provide liquidity, then earn from:

- Fee accrual on BULX

- Revenue share and staking APY on PAI

- A Loss Protection Program that scales from 50% to 100% coverage over 90 days

The site highlights an A.M.M.Q Engine (Automated Market Making something) that handles rebalancing, liquidity, and spreads automatically. It claims low latency and high uptime. An insurance pool shows $12.4 million, listed as 4.2% of TVL. Simple math puts implied TVL near $295 million.

Promoters outside the main site go further. Some videos and posts talk about daily returns from 3.5% up to 20%. These numbers appear in tutorials linked to registration codes and referral activity. The official site stays more technical and avoids exact daily percentages, but the overall message pushes high, consistent yields through staking and protection features.

No clear MLM structure (binary legs, matrix boards, or rank charts) shows up in public materials. Promotion leans on referral codes, Telegram groups, and network-style onboarding. You earn through token rewards and possible revenue share rather than fixed commission levels.

Customer support runs mainly through Telegram and an X account (@Uniko_L3). Payment happens via crypto deposits to smart contracts. No fiat options or regulated banking rails appear.

Part 2: Why the Numbers Raise Questions: Simple Math Anyone Can Follow

High returns sound exciting, but basic math shows why they can be hard to sustain long term.

Take a modest 2% monthly return (about 26% APY). Start with $1,000,000 in deposits. The platform needs $20,000 that month just to pay existing users. Without real trading profits, new money must cover it. Next month, the bill grows because the new deposits also earn returns. Over time, this creates an ever-rising need for fresh capital.

The insurance pool math adds another layer. With $12.4 million covering 4.2% of TVL, a full loss would leave a huge gap. Even 50% protection requires far more reserves than shown.

Here is a quick comparison table of realistic returns versus the kind of claims floating around:

Investment Type | Typical Annual Return | Risk Level | Transparency |

Bank savings or fixed deposits | 3–6% | Very low | High |

Real estate (rental + growth) | 6–12% | Low to medium | High |

Regulated crypto staking | 5–15% | Medium | High |

Claimed high-yield promotions | 300%+ (or daily %) | Very high | Low |

Figure 1: Growth comparison (imagine a line chart here). A steady 10% annual line rises slowly and smooth. A 2% monthly compound line shoots upward fast, reaching thousands of percent in a few years. Real markets do not deliver that without huge risk or outside money flowing in.

Another example: 1% daily compounds to roughly 3,678% in one year. That beats every major index, hedge fund, or bank by a mile. History shows most schemes promising these levels rely on new deposits to pay old ones. When inflows slow, payouts stop.

2.1 Platform Features, Traffic, and Public View

The site looks modern with clean design and technical jargon. It lists big names as partners (CertiK, Chainlink, Jump Trading, even Alameda Research). Yet independent checks find no public confirmation of audits or current partnerships from those firms. Alameda’s well-known 2022 collapse makes its listing especially hard to understand in 2026 materials.

Traffic data stays low or unavailable. No strong presence appears on major DeFi trackers. The linked app domain feels very new and carries mixed trust signals on review tools.

Social channels exist (@Uniko_L3 on X, t.me/UnikoL3 on Telegram with a few thousand members). Promotion mixes tutorial videos and referral talk. Some promoters have ties to other short-lived projects.

No major red flags from regulators yet, but the lack of licenses, named team, and verifiable on-chain proof stands out.

Key Red Flags Summarized in Bullet Points

- Ownership stays mostly hidden behind a new holding company with small capital and limited experience.

- No public team bios or verifiable executives.

- High yield language appears in promotions even if the site stays technical.

- Insurance and protection claims do not fully match the math.

- Partner logos lack independent proof.

- Promotion relies on referrals and network-style growth.

- Very new app domain with privacy protection.

Practical Advice Before You Decide

Look closely before sending any funds. Ask for named leaders, full company filings, live on-chain reserve proof, and independent audit links. Test small if you must, but only what you can afford to lose. Watch for withdrawal issues, which often appear when new money slows.

The platform offers an interesting concept around liquidity and protection. Real DeFi can work when built on solid ground. Right now, the gaps in transparency make it feel high-risk.

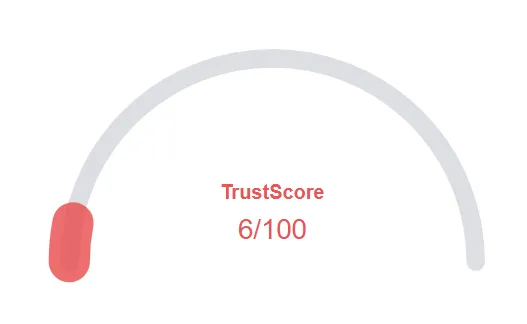

UNIKO Review Score

A website’s trust score is an important indicator of its reliability. UNIKO includes low web traffic, negative user feedback, potential phishing risks, undisclosed ownership, unclear hosting details, and weak SSL encryption.

With such a poor trust score, the likelihood of fraud, data breaches, or other security issues is much higher. It is crucial to carefully assess these warning signs before engaging with a UNIKO or similar platform.

Positive Highlights

- We found a valid SSL certificate

- DNSFilter labels this site as safe

Negative Highlights

- The Tranco rank (how much traffic) is rather low.

- The age of this site is (very) young.

Frequently Asked Questions UNIKO Review

This section answers key questions about UNIKO clarifies points, addresses concerns, and highlights issues related to the platform’s legitimacy.

Transparency is limited. Without clear owners and proof of reserves, many view it as high risk. Always verify independently.

Rewards come through token staking, fees, and the protection program. Exact daily or monthly rates are not fixed on the site but appear in external promotions.

Linked to a Swiss holding company run by two directors with no public record in large-scale trading or crypto.

Math shows such high figures are hard to sustain without constant new capital. Compare against bank or market benchmarks.

Review the Swiss company register, search for audit reports on CertiK’s site, and monitor Telegram and X for real user experiences over time.

Other Infromation:

WHOIS Last Update Date: N/A

Reviews:

There are no reviews yet. Be the first one to write one.